Do you want to start saving $1,000 a month, but you only make $50k a year? It may feel out of reach, but I promise that it is possible.

I make $53k a year and have been saving $1,000 a month for the last few years. It wasn’t easy at first, but over time, I’ve picked up some tips and tricks that have made saving money effortless.

In this post, I’ll share how to create a savings plan and 8 tips for saving money on a $50k salary!

Is Saving $1,000 a Month on a $50K Salary Possible?

Is saving $1,000 a month on a $50k salary actually possible? Let’s find out.

If you make $50k a year, your approximate monthly take-home income is $3,513.25. Keep in mind that if you live somewhere with state income tax, your take-home income will be lower.

Saving $1,000 a month on a take-home income of $3,513.25 means you’re saving approximately 31.5% of your income. This isn’t impossible per se, but it’s well above the average personal saving rate in the U.S., which is currently 3.4%, according to Money Geek. It’s also 11.5% higher than the common savings recommendation of 20%.

With this being said, saving $1,000 on a $50k salary is possible — I mean, I’m doing it! But you will need to seriously change your spending habits and mindset surrounding money. Luckily, that’s what we’ll be discussing in this post.

5 Steps to Prepare to Save $1,000 a Month

Like most things in life, planning is crucial for success. You can’t expect to change your spending and saving habits without putting in some work and preparation upfront.

To prepare for this money-saving journey you’re about to embark on, you’ll want to create a savings plan. Here’s how.

1. Set Clear Savings Goals

Step 1 is simple: you’ll want to set clear savings goals. Since you clicked on this post, I’ll assume that your goal is to save $1,000 a month. However, let’s take this goal a step further. Instead of just deciding how much you want to save, ask yourself why you want to save. Having clear motivations in mind will help you stick with your savings plan even when faced with temptation.

Your savings goals may include saving up for a new car or building an emergency fund. Perhaps you have various savings goals. If you have multiple goals, ask yourself which ones are your priority and how much money you’d like to allocate per goal.

For instance, let’s say you want to pay off your debt, max out your annual Roth IRA contribution, and build an emergency fund. Prioritize your savings goals so that you know exactly where your money is going. In the example above, I’d recommend paying off your debt first, then building an emergency fund, and lastly contributing to your Roth IRA. When it comes to money, the goal is to avoid paying interest. So, if you can pay off your debt quickly and also build up an emergency fund (so you don’t need to get further in debt), that should always be the priority.

2. Track Your Expenses

After you’ve set your goals, it’s time to track your expenses. Tracking your expenses is crucial if you want to understand exactly where your money is going and why. It’ll give you a clear picture of your financial habits so that you can identify areas where you can cut back.

I recommend looking back at your last 3-6 credit card statements. Count up all of your expenses and separate them into different categories like rent, groceries, clothing, subscription services, medical bills, etc. Track each month’s expenses separately so that, in the end, you can compare each month and get an idea of your average monthly spending.

It may look something like this:

Month 1:

- Rent: $850

- Groceries: $250

- Cellphone: $60

- Electricity/Water/Gas: $250

- Health Care: $31

- Public Transportation: $100

- Eating Out: $209

- Clothing: $80

Total Expenses: $1,830

Month 2:

- Rent: $850

- Groceries: $300

- Cellphone: $60

- Electricity/Water/Gas: $250

- Health Care: $31

- Public Transportation: $100

- Eating Out: $150

- Clothing: $120

Total Expenses: $1,861

Month 2:

- Rent: $850

- Groceries: $180

- Cellphone: $60

- Electricity/Water/Gas: $250

- Health Care: $31

- Public Transportation: $50

- Eating Out: $50

- Clothing: $0

Total Expenses: $1,471

If you make $50k a year, that means your take-home income is $3,176 (if you don’t have state income tax, aren’t contributing to a retirement plan, HSA, or have any other automatic deductions.)

So, if you want to save $1,000 a month, you will want to try to keep your monthly expenses under $2,000.

3. Create a Budget

When it comes to saving money, there’s no secret formula. If you’re currently saving $0 a month but want to save $1,000 a month, you’ll need to spend $1,000 less each month. You may be thinking, ‘but how?!’ The answer lies in creating a budget.

A budget outlines how much you’re able to spend on various expenses throughout the month. Keeping a budget allows you to manage your money effectively and track your spending so that you can reach your financial goals and stop overspending.

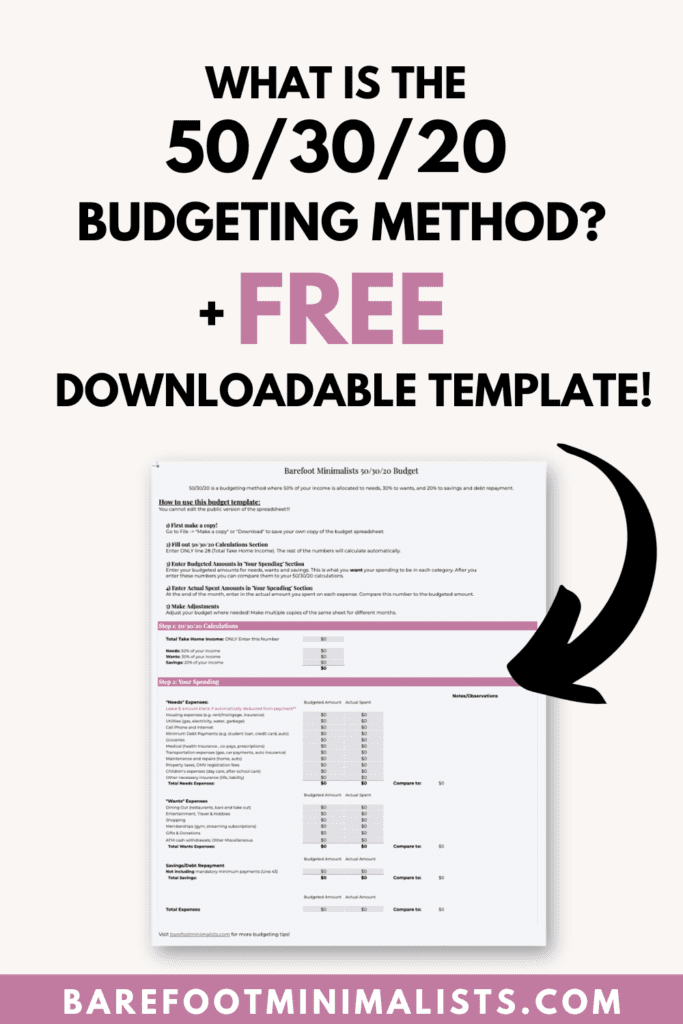

There are many different budgeting methods out there, from the 50/30/20 rule to zero-based budgeting. You can choose to use a budgeting app to track your spending, a spreadsheet, or good old-fashioned pen and paper. I use this 50/30/20 budgeting template for my personal budget. If you’re not sure how to organize your budget, here are over 100 budget categories and subcategories to include in your personal budget.

Later in this post, I’ll give you some tips for lowering your expenses (even the expenses you think won’t budge!)

4. Open a High-Yield Savings Account

After you’ve created a budget, you’ll need a place to store your savings, and there’s no better place than in a high-yield savings account.

A high-yield savings account is a type of savings account that offers a higher interest rate compared to traditional savings accounts. Instead of earning 0.01% interest, as you would with many traditional brick-and-mortar bank savings accounts, you could earn closer to 4 or 5% interest! These accounts are typically offered by online banks, credit unions, or financial institutions that operate with lower overhead costs, which is why they’re able to offer higher interest rates.

Saving money in a high-yield savings account can be way more encouraging than saving money in a typical savings account. Seeing your savings balance go up on a regular basis can be a great motivator for saving and can help you stick with your savings goals. Plus, having your savings account separate from your checking account means moving money between accounts will take a couple of days (instead of automatically), which can help you curb impulse purchases. If you have trouble controlling the impulse to transfer money out of your savings account into your checking account, opening a high-yield savings account can work wonders.

I keep my emergency fund in the Marcus by Goldman Sachs online savings account, which earns a 4.50% annual percentage yield (APY). Interested in opening an account? Click here to sign up using my referral code and earn an extra 1.00% APY for the first 3 months.

If you already have an emergency fund saved up, you may be interested in investing your savings instead. If so, click here for a beginner-friendly guide to investing.

5. Automate Your Savings

The last step before we get into the tips is to automate your savings. Instead of relying on yourself to transfer $1,000 a month into your savings account, make this an automatic process so you don’t even have to think about it. Keep in mind that if it’s automatic, you’ll need to be extra conscious of your spending throughout the month to ensure that your transfer goes through. This is both a good and bad thing. If you overspend, you may risk an overdraft fee from your bank. On the plus side, the threat of needing to pay a fee, may help you stay committed to your savings goals.

8 Tips to Save $1,000 a Month on a $50K Salary

Now that you’ve done everything you need to prepare for saving $1,000 a month on a $50k salary, it’s time to share the tips that’ll help you get there.

Here are 8 tips to help you cut back on your spending so you can save money.

1. Cut Unnecessary Expenses

As you were tracking your expenses, did you notice any areas where you were spending money on things that you don’t actually need? If you want to start saving $1,000 a month, you’ll want to prioritize your needs over your wants. So, start by analyzing your spending for areas where you can cut back—think dining out, subscription services, and unnecessary clothing purchases. I find it helpful to actually write a list of all my ‘needs’ (necessary spending) and ‘wants’ (unnecessary spending). This helps me visualize exactly where my money is going.

When you prepare your budget, make sure that you are either allocating way less money toward these expenses or just cutting them out entirely.

If cutting out all unnecessary spending seems like a big lift, cut out one thing at a time. In your first month of budgeting, cut out (or seriously limit) the amount of money you can spend on dining out. In your second month, cut out clothing shopping. By slowly tapering down your spending, it’ll feel way more sustainable and less shocking to spend less.

Tips to save money on “unnecessary” expenses

- Order water at restaurants instead of soda or tea.

- Go to thrift shops instead of buying new.

- Learn to cut or style your hair at home.

- Borrow books, movies, and magazines from the library instead of buying them.

- Instead of going out with friends, organize potluck dinners or game nights at home.

2. Lower Your Biggest Expenses

Next, take a look at the expenses that you would categorize as “needs” – things like groceries, rent, transportation, and bills.

If your goal is to challenge yourself to save $1,000 a month on a $50k salary, you’ll need to brainstorm creative ways to lower these expenses too (especially since they’re typically your biggest expenses). You might assume that these expenses are fixed, but in reality, there are plenty of ways to reduce them.

There are things you can do to cut these expenses out entirely, like moving in with your parents to eliminate rent or choosing to walk everywhere to cut transportation costs. However, these major changes can significantly impact your quality of life or may simply not be feasible given your personal circumstances.

So, let’s brainstorm some ways to lower your biggest expenses without totally uprooting your life.

Tips to Save Money on Rent/bills

- Explore alternative housing options like co-living spaces or basement suites.

- Sign an extended lease.

- Get a roommate.

- Give up your parking spot.

- Lock in your natural gas rate.

Click here for 50 Frugal Tips to Save Money on $1500 a Month.

Tips to save money on groceries

- Cook at home and meal prep.

- Use up all products and food items (before buying more).

- Buy generic over name brand.

- Don’t shop hungry.

- Make use of food pantries in your community.

Click here for 21 Ways to Save Money on Groceries.

TIps to save money on transportation

- Research what the cheapest gas stations are in your area (mine are Arco and Costco).

- Use public transportation or carpool.

- Downgrade your vehicle.

- Earn $100 to $500 a month wrapping your car with advertising.

- Bike or walk instead of drive.

Click here for 50 Unusual Frugal Tips You’ll Wish You Knew Sooner.

3. Analyze Your Shopping Habits

Another tip to save $1,000 a month on $50k a year is to analyze your shopping habits.

Where you shop, how you shop and when you shop can make a huge difference in how much you spend and save each month.

As far as when you shop, here are some things to consider:

- Never grocery shop when you’re hungry.

- Shop for groceries on Wednesdays and Thursdays (these days have the biggest sales!)

- Don’t shop if you’re feeling stressed out, anxious, or sad.

- Instead of doing a big grocery haul every few weeks, try shopping more frequently. This will save money on food waste.

As far as where you shop, here are some things to consider:

- Make more than one stop while grocery shopping to get the best deals. (For instance, go to Costco for bulk items and somewhere else for fresh foods.)

- Avoid grocery shopping at stores that might temp you to buy things other than groceries. I avoid going to Target because I find that even if I plan to buy one thing, I often leave the store with a cart full of items that I was never intending on buying.

- Shop at extreme value grocery stores, such as Grocery Outlet.

- When it comes to buying clothing, go to thrift stores instead of buying new. My favorite way to buy clothing is to sell pieces I don’t wear anymore at a consignment shop and use the store credit to buy new pieces (it’s technically free!)

As far as how you shop, here are some things to consider:

- Order Groceries through pickup/drive up. This can help you plan and be more intentional with your purchases. Plus, you’ll be less tempted to pick up random things that you weren’t intending on buying.

- Notice whether you spend less when you shop online or in person. I find that shopping online triggers impulse purchases but shopping in person does not. So, I try and shop in person when I can.

- Cash or card? Ask yourself if you spend less when you spend cash or card. For me, cash feels like Monopoly money and I tend to spend it way more carelessly, so, I avoid taking out cash at all and put all purchases on my credit card. I’ve heard some people say the opposite – that they spend less when they have to hand physical cash over because it feels more immediate. Notice your own habits.

4. Prioritize Your Mental Health and Well-Being

When I’m not doing well mentally, I’m way more likely to overspend. There’s actually a scientific reason behind why this is happening.

Spending money releases feel-good chemicals like endorphins, serotonin, and adrenaline that temporarily dull any negative feelings you may be experiencing. Of course, those feelings come back as soon as the excitement of the purchase wears off, but by then it’s too late, and the money has been spent.

So, if you’re trying to save money, the best thing you can do is prioritize your mental health and well-being. The happier and more content you are, the less likely you are to use shopping as a way to self-soothe. If you feel genuinely filled up by life, experiences, and love, you won’t chase the high of spending money because you’ll be getting that high from life itself.

As I’ve been prioritizing saving money, I’ve also been prioritizing my mental health and well-being. I’ve been doing this by keeping up with my wellness practices and prioritizing my energy givers like moving my body and spending time in nature.

5. Make Impulse Purchases Harder

If you want to save $1,000 a month on a $50k salary, you’ll want to get a handle on your impulse purchases.

Impulse purchases are the ones you make that are not thought out or budgeted for. They can be as innocent as picking up a few extra goodies at Target or as serious as making a major purchase without thinking it through.

To curb those impulse purchases, you’ll want to set up barriers to make it harder to shop impulsively.

Here are several ways to make impulse shopping harder:

- Start a wish list on your phone or in a notepad. If you have the impulse to buy something you don’t need, write it on this list. Wait 30 days before buying it. Most of the time, you’ll find that the impulse to purchase this item has passed!

- Turn on grayscale mode on your phone. Grayscale mode turns the way colors are displayed on your phone into shades of gray, making it almost impossible to online shop, especially for clothing. Think about it: how can you buy a shirt if you don’t even know what color it is?

- Don’t save your credit card information. Needing to add your credit card information every time you want to make a purchase creates a barrier that’ll slow down your online shopping and give you a moment to consider whether you should really make the purchase.

- Stop following social media influencers who encourage you to shop. Instead, follow minimalist influencers that encourage you to live with less and be grateful for what you have. Click here to discover 10 of my favorite minimalist bloggers.

For more tips to help you stop shopping impulsively, click here.

6. Explore Free Hobbies and Activities

Think about what you do in your spare time. If your idea of a fun time is shopping, eating out at restaurants, or clubbing, you’ll need to open your mind to free hobbies and activities if you want to save money.

If you like going out to eat, consider hosting a potluck with friends as a low-cost alternative. Instead of clubbing, have a dance party at home. If you love shopping for clothing, host a clothing swap where all your friends bring clothing pieces they no longer wear and trade with each other.

My favorite free hobbies and activities include painting, working out, and having tea dates at home with my friends. I find that spending money on a gym membership actually allows me to spend less in the long run. I spend $70 a month on a membership, but that gives me an activity to do almost every day. I’ve even started working out with friends to make it more social and fun.

7. Travel on a Budget

I LOVE to travel, but I don’t want a single trip to set me back thousands of dollars. Over the years, I’ve really been able to nail down what budget travel means to me. Although I’m not staying in the most luxurious hotels, I’m able to travel way more often and stick to my saving goals.

Here are some tips for budget travel:

- Create a travel budget! Click here to learn how.

- As far as activities go, I treat travel like my day-to-day life and do things that I already love to do but just in a new environment. Instead of going sightseeing every day, I spend a lot of time going on long walks, runs, doing yoga at the park, and just simply exploring.

- If I’m traveling somewhere warm, I always try and camp at least some nights. A) It’s so much more adventurous, and B) it saves me so much money! Freecampsites.net is a great resource for free camping. Keep in mind that you may be charged extra fees for flying with your camping gear for checking in larger bags. I’m able to fit everything into my backpacking backpack, which is small enough to bring on the plane as a carry-on!

- I stay at hostels instead of expensive hotels and Airbnb‘s. It’s way cheaper and I’ve met so many interesting people traveling this way.

8. Sell or Rent Things You Don’t Use

Remember how I said that in order to save $1,000 a month you’ll need to spend $1,000 less each month? Well, there’s actually a way to skirt around that – by making some extra money to supplement your salary.

There are a few ways to do this. You can:

- Start a side hustle. Click here for 18 side hustle ideas.

- Generate passive income. Click here for 11 passive income ideas (that you don’t need initial funds for).

- Sell or rent things you don’t use.

Because I’ve already written two in-depth posts about side hustles and passive income streams, I’m not going to go into more detail about that now. Instead, let’s discuss how you can make money by selling or renting things you don’t use.

My friend rents out her garage for $500 a month. She put an ad on Facebook Marketplace and was able to connect with an athlete who had tons of outdoor gear but didn’t have the space to store it. If you also have a garage that isn’t being used (or that you can clear out), I highly recommend renting it out. After all, if you can earn an additional $500 a month, that’s half of your savings goals right there!

If you live in an apartment and don’t have a car (or don’t mind parking on the street), renting out your parking spot may be a great option for you. Just make sure to check in with your leasing manager first.

If you own a car that you don’t use every day, you can rent it through companies like Turo and Getaround. According to Turo, the average annual income of someone renting out 1 car is $10,516 – that’s just short of $12,000!

These are just a handful of the many ways you can make extra money selling or renting out your unused things. If none of these apply to you, get creative! You’d be surprised by how many people are looking to rent a lawnmower, skis, a bike, or thousands of other items instead of buying it themselves. My favorite spots to rent or sell my unused things are Facebook Marketplace, Offerup and eBay.

Saving $1,000 a Month on a $50K Salary

Saving $1,000 a month on a $50k salary isn’t easy, but it is possible. It boils down to setting yourself up for success with a solid budget, a high-yield savings account, and automating your savings to make it effortless. After that, embracing the 8 tips mentioned above can help you save money on your necessary and unnecessary expenses so that you can allocate more money towards your savings goals!

Are you currently trying to save money on a low income? Let’s all help each other in the comments below by sharing our most effective money-saving tips!

Leave a Reply